7 Virtual Data Room Mistakes That Cost Sellers Millions in Due Diligence (2026)

7 Virtual Data Room Mistakes That Cost Sellers Millions in Due Diligence (2026) Most sell-side advisors understand, at least in principle, that a disorganized virtual data room is bad for a transaction. What is less understood — and what costs sellers real money — is how specific, avoidable erro

7 Virtual Data Room Mistakes That Cost Sellers Millions in Due Diligence (2026)

Most sell-side advisors understand, at least in principle, that a disorganized virtual data room is bad for a transaction. What is less understood — and what costs sellers real money — is how specific, avoidable errors translate directly into buyer leverage, valuation adjustments, and deal delays that compound across the weeks of a live process.

The mistakes listed here are not hypothetical. They are the patterns that appear repeatedly across lower-middle-market sell-side processes, often from sellers who believed they were prepared.

In each case, the error was identifiable and remediable before the first buyer NDA was signed. In each case, it was not caught in time.

If you are an advisor preparing a client for a sale process, or an owner who is twelve to eighteen months from a planned exit, read this before you open the data room to anyone.

Free Resource: Before your VDR goes live, run a complimentary due diligence evaluation report to identify document gaps and structural issues your team can address before buyer access begins.

Why VDR Errors Are the Most Preventable Source of Deal Friction

There is an important distinction between diligence problems that are inherent to the business — customer concentration, a key-person dependency, a pending regulatory matter — and problems that exist solely because of how the data room was set up. The first category requires strategic management.

The second category requires only preparation and process discipline.

In our experience across sell-side advisory engagements in the lower-middle market, VDR execution errors consistently fall into the second category. They are not caused by bad businesses.

They are caused by advisors who treated the data room as an administrative afterthought rather than a strategic asset.

The buyer's diligence team, particularly in PE-backed processes, is trained to look for patterns. A disorganized data room, a document naming inconsistency, a folder that is half-populated — these signals aggregate in the buyer's mind into a risk narrative about the business.

That narrative does not require any single damning finding. It just requires enough accumulated friction to justify a conversation about price.

What We Actually See In Deals: The most expensive VDR mistakes are not usually the dramatic ones — a leaked customer list or an unredacted trade secret. They are the quiet ones: a financial statement that does not tie to the EBITDA bridge, a contract that was uploaded but never checked for change-of-control language, a tax return that covers three years but skips one amended state filing. Each item, on its own, might be explained away. Together, they build a buyer's case for a lower number.

Case Studies: Two Deals, Two Entirely Different Outcomes

Case Study: The Folder That Stalled a Deal for Six Weeks

An advisory team we know of was running a sell-side process for a Midwest business services company. The initial buyer interest was strong, and three groups submitted indications of interest within the first four weeks.

One of those groups, a regional PE firm with a strong track record in the sector, was clearly the most qualified buyer and had submitted the most favorable preliminary terms.

During confirmatory diligence, the PE firm's legal team flagged a problem. The company's material vendor agreements — specifically a data processing arrangement that was essential to the core service delivery — were stored in a folder labeled "Contracts - Misc." alongside expired NDAs, old lease addenda, and two documents that appeared to be unrelated to the business entirely.

The vendor agreement itself was fine. The terms were standard and transferable.

But finding it, verifying it was the correct version, and confirming it had no embedded change-of-control restriction took the buyer's legal team three separate document requests, two weeks of back-and-forth through the Q&A module, and one direct attorney call to resolve. The buyer's confidence in the operational documentation of the business was shaken.

The deal closed. But the exclusivity period was extended twice, the seller's legal fees increased substantially, and the buyer negotiated a working capital adjustment that might have been avoided had the process moved more efficiently.

The advisor estimated that the organizational failure cost the seller more than the entire cost of a properly configured VDR platform would have over the life of the process.

How It Should Be Done: A Pre-Launch Audit That Changed the Outcome

A contrasting situation involved a Southeast technology services company preparing for its first institutional capital raise. The founders had never been through a formal diligence process and were initially resistant to the time required for pre-launch VDR preparation.

Their advisor insisted on a structured pre-launch audit. Over eight weeks, the team identified several gaps: two customer contracts operating under expired MSAs, an IP assignment agreement with a freelance developer that had never been executed, and a state tax filing from two years prior that had been amended but whose amended return had not been filed in one jurisdiction.

All three issues were resolved before the data room launched. The IP assignment was documented retroactively with the developer, who was still reachable.

The amended tax return was filed. The customer contracts were updated with formal extensions.

When the buyer's team entered the VDR, the process moved at a pace the founders described as faster than they had anticipated. The buyer found nothing that required explanation.

The deal closed on the originally projected timeline, above the initial valuation range discussed during the engagement kickoff.

The lesson was not that the business was in better shape than it appeared. It was that the pre-launch preparation had already done the work that would otherwise have been done under buyer scrutiny — at a much higher cost.

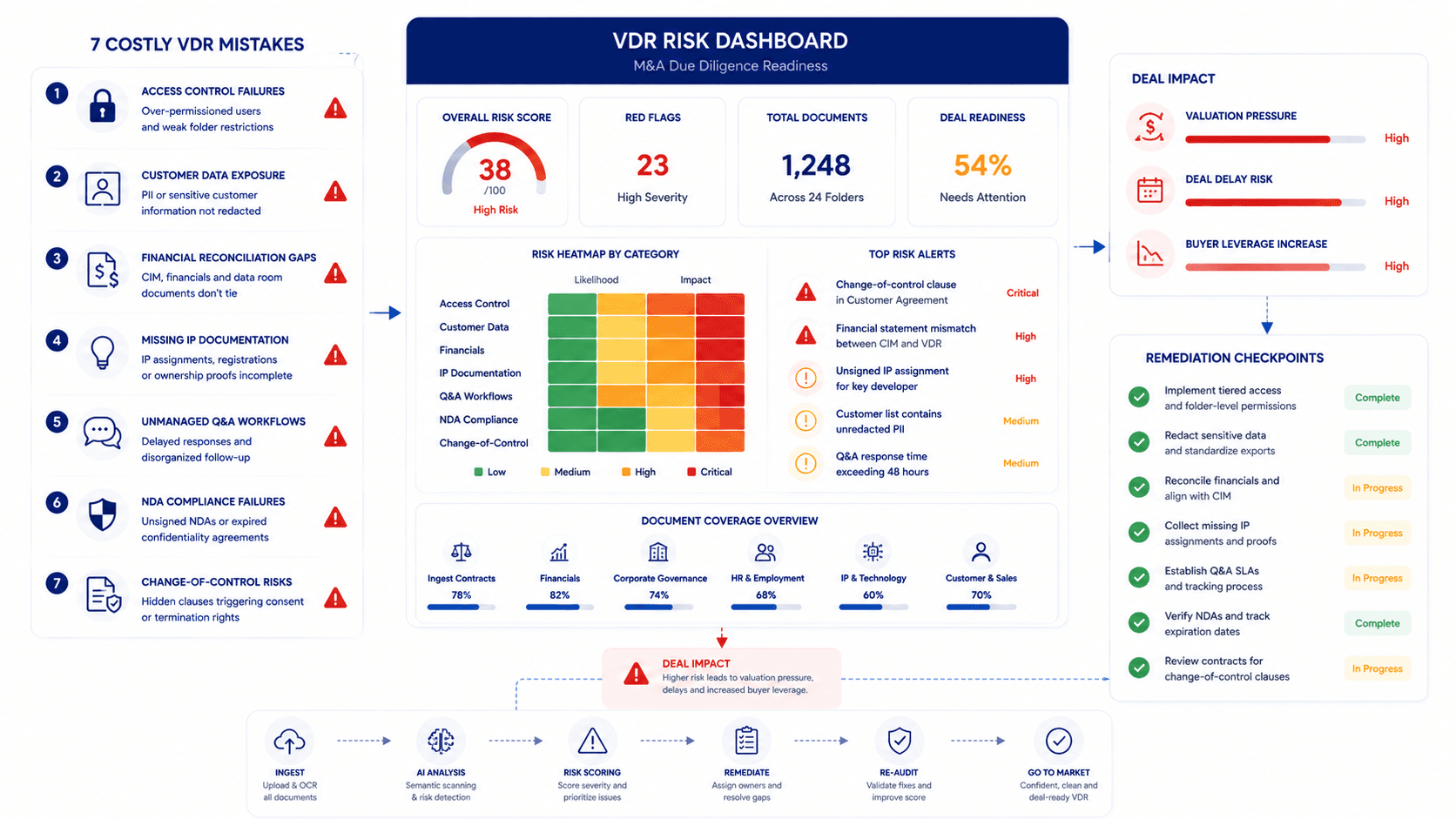

The 7 Most Costly VDR Mistakes in 2026

Mistake 1: No Tiered Access Control from Day One

This is the foundational error. Many advisory teams configure the VDR with a single access level for all buyers, allowing every NDA signatory to see every document simultaneously.

The logic is simplicity — managing tiered access takes time, and early-stage buyers do not always need the most sensitive materials.

The problem is that early-stage buyers are often the least vetted. A strategic acquirer who is also a direct competitor may have signed your NDA specifically to gather intelligence on customer relationships, pricing structures, or key personnel.

Without tiered access, there is no mechanism to release sensitive information only to buyers who have demonstrated serious intent by submitting a letter of intent.

Configure Tier 1 — financial summaries, the CIM, high-level organizational materials — before launch. Hold Tier 2 materials for IOI-stage buyers.

Reserve Tier 3 for LOI-stage confirmatory diligence only. The buyer who eventually transacts will have earned full access.

The buyer who does not transact will have seen only what you would have shared in any marketing conversation.

Mistake 2: Uploading Unredacted Customer Concentration Data

Customer concentration is one of the most common valuation discount triggers in lower-middle-market M&A. Buyers adjust their risk assessment — and their price — when a significant portion of revenue is concentrated in a small number of relationships.

That adjustment is a legitimate part of the negotiation. What is not legitimate — and what costs sellers leverage — is allowing buyers to quantify the concentration risk before the advisor has contextualized it.

An unredacted customer schedule showing that one client represents a substantial portion of trailing revenue, uploaded without any accompanying retention documentation or renewal timeline, hands the buyer a discount argument before any management presentation has explained the relationship's durability.

Redact customer names in all Tier 1 and Tier 2 materials. Replace them with coded identifiers (Customer A, Customer B).

Provide concentration percentages by revenue tier, but not by named account. Release unredacted customer-level data only to the buyer under LOI, accompanied by supporting materials that document contract terms, renewal history, and relationship tenure.

Mistake 3: CIM Financial Figures That Don't Match the VDR

This mistake is both common and immediately damaging. The CIM presents normalized EBITDA of, say, $2.8M on a specific add-back basis.

The VDR contains three years of QuickBooks exports, a payroll summary, and a ledger-level adjustments schedule — but the math in the adjustments schedule does not produce the same EBITDA figure that appears in the CIM.

Buyers are not charitable about discrepancies like this. Even if the difference is explainable — a different treatment of a one-time item, a rounding convention, a period adjustment — the mismatch creates doubt about the reliability of the entire marketing package.

In our experience, the discovery of a CIM-to-VDR discrepancy is one of the most reliable triggers for a buyer requesting an independent quality of earnings review at the seller's expense.

Before the VDR launches, have an advisor or accountant reconcile every financial figure in the CIM against the source documents that will appear in the data room. Every EBITDA add-back must be traceable to a specific document in the financial records folder.

Every revenue figure must tie to the monthly management accounts.

Mistake 4: Missing or Informal IP Documentation

For any business where technology, proprietary processes, or brand reputation represent a meaningful portion of enterprise value, intellectual property documentation gaps are a diligence landmine. The issue is rarely that the IP does not exist — it is that its ownership has never been formally documented.

Software companies frequently have code contributions from freelance developers who were never asked to sign IP assignment agreements. Professional services firms may have developed proprietary methodologies that were described in marketing materials but never formally protected.

A product business may have a patent pending but no formal assignment from the individual inventor to the operating entity.

Each of these gaps, when discovered during confirmatory diligence, triggers a legal review, a cure period, and often a representation and warranty carve-out or escrow demand. Many are curable in advance if identified early.

Virtually none are curable in 48 hours while a buyer's legal team is waiting.

Audit IP ownership documentation as a pre-launch priority, not a confirmatory diligence item.

⚠️ Common Mistake: Uploading core IP documentation — detailed source code, proprietary algorithm specifications, unpatented trade secrets — to the general VDR folder accessible to all early-stage buyers. Strategic buyers may be direct competitors. Restrict all detailed technical IP to a clean-team-only folder accessible only to outside legal counsel for the buyer, released exclusively during final confirmatory diligence.

Mistake 5: No Q&A Log Discipline

Most purpose-built VDR platforms include a Q&A module that routes buyer questions to designated advisors for response. Many advisory teams bypass this module and allow buyers to email questions directly.

This feels more efficient in the short term.

It is not.

When questions are answered via email, there is no central record of what was asked, what was answered, and when. If two buyers ask the same question and receive slightly different answers, the inconsistency becomes a material disclosure issue under representations and warranties.

If a buyer later claims they were not told something that was communicated verbally or via email, the absence of a VDR log makes the dispute harder to resolve.

Run all buyer Q&A through the VDR module. Route questions to the appropriate advisor by category — financial questions to the lead advisor, legal questions to counsel.

Set response time standards and enforce them. The Q&A log produced by the platform at closing is part of the transaction's disclosure record.

Mistake 6: Granting VDR Access Before the NDA Is Fully Executed

This seems obvious. It is also, in practice, violated regularly.

Advisory teams eager to maintain buyer momentum sometimes allow early document access while the formal NDA is "in review." The buyer's associate has already asked for the CIM. The NDA is a formality.

The relationship has been established over several calls.

None of that context matters if something goes wrong. An NDA executed after document access has begun is a significantly weaker instrument than one executed before.

In some states, confidentiality obligations that attach after the disclosure of information may be unenforceable with respect to that information.

Gate VDR access behind a fully executed NDA. Use the VDR platform's access invitation workflow, which can be tied to confirmation of NDA receipt. This is not a formality.

Mistake 7: Ignoring Change-of-Control Provisions in Material Contracts

Under standard commercial contract law and federal antitrust guidelines, many agreements — particularly enterprise customer contracts, key vendor relationships, and financing arrangements — contain provisions that require the counterparty's written consent before the agreement can be assigned to a new owner. In heavily regulated industries, government contracts and professional licenses may also require regulatory approval of the change of ownership.

Advisory teams routinely upload material agreements to the VDR without first reviewing them for assignment restrictions. When the buy-side legal team identifies a change-of-control clause requiring consent — especially in a contract representing a significant revenue relationship — the transaction timeline is extended while consent is obtained, and the buyer gains leverage to demand protective provisions in the purchase agreement.

Review all material contracts for change-of-control language before the VDR launches. Catalogue every agreement that requires consent.

Develop a consent strategy — in some cases, the seller should initiate the consent process proactively with the counterparty before the buyer is aware of the contract. According to FTC premerger guidance, certain transactions may also trigger notification obligations that are distinct from individual contract consent requirements.

Reactive Remediation vs Proactive VDR Audit: A Side-by-Side Comparison

Reactive Remediation (Fixing Problems During Buyer Diligence)

- Timing: Problems identified after buyers have entered the VDR

- Buyer Impact: Each gap triggers a formal document request, extending the Q&A cycle

- Negotiating Position: Seller is explaining problems under scrutiny; buyer has leverage

- Legal Exposure: Ad hoc fixes may be challenged as inadequate in post-closing indemnification

- Timeline: Each unresolved item adds days to weeks to the closing schedule

- Cost: Legal fees, advisor time, potential escrow holdbacks, and valuation compression

Proactive VDR Audit (Pre-Launch Gap Identification and Remediation)

- Timing: Gaps identified three to six months before buyer access begins

- Buyer Impact: Buyers find a complete, organized VDR with no unexplained gaps

- Negotiating Position: Seller demonstrates institutional discipline; buyer has less leverage

- Legal Exposure: Documented remediation creates a defensible pre-closing disclosure record

- Timeline: Process moves at projected pace; exclusivity period is typically shorter

- Cost: Advisory time and platform subscription; significantly lower than reactive remediation costs

How AIVI Flags VDR Risk Signals Before Buyers Do

The seven mistakes described in this article share a common characteristic: they are all detectable before the data room opens. What prevents detection is the absence of a systematic process for identifying and tracking document gaps across all diligence categories simultaneously.

Advisory teams using the VDR remediation Kanban at AIVI run this process as an integrated workflow rather than a manual checklist exercise. When a client completes the exit readiness diagnostic, the platform generates a structured gap analysis across corporate legal, financial records, customer contracts, IP, HR, and compliance categories — the same categories that will eventually form the VDR's folder structure.

Each identified gap becomes an assigned task on the remediation board, with an owner, a target date, and a status that both the advisor and the client can see. The seven mistakes described above correspond directly to task categories in the remediation workflow: access control configuration, customer data redaction review, CIM-to-VDR financial reconciliation, IP ownership audit, change-of-control contract review.

The automated CIM generation feature ensures that the financial figures in the marketing package and the financial documents in the VDR originate from the same diagnostic data, eliminating Mistake 3 entirely before the first buyer conversation begins. You can review a sample of how the full complete VDR due diligence checklist integrates with the remediation workflow in our related guide.

Frequently Asked Questions

What is the most common virtual data room mistake sellers make?

The most common mistake, in our experience, is launching a VDR without tiered access control. Many advisors configure a single access level for all buyers, allowing every NDA signatory to see all documents simultaneously.

This exposes sensitive materials — customer lists, personnel compensation, IP documentation — to buyers who may be competitors or who may not ultimately transact. Tiered access, configured before launch, is the single most important structural safeguard in a sell-side data room.

Can a disorganized VDR actually affect the purchase price?

Yes, and it frequently does. Buyers use the organization and completeness of the data room as a proxy for the operational discipline of the management team.

A chaotic VDR signals risk, and buyers quantify risk through purchase price adjustments, indemnification escrow demands, and working capital peg negotiations. In our experience, VDR-related friction is one of the most reliable predictors of extended exclusivity periods and post-LOI retrading of price.

How do you fix a change-of-control clause problem discovered during diligence?

When a change-of-control clause is identified during active buyer diligence, the sell-side legal team must immediately assess whether the consent requirement is a condition to closing or a breach right. If it is a condition, the advisory team initiates a consent request process with the counterparty, typically managed by outside counsel and coordinated with the buyer.

The buyer's legal team will typically request a representation in the purchase agreement addressing the consent status, and may require an indemnification escrow for any contract where consent has not been obtained by the closing date.

Should sellers upload all documents to the VDR before the first buyer NDA is signed?

No. The data room should be built and ready to launch before the first NDA, but buyer access should be gated behind a fully executed NDA.

Many advisors prepare the full Tier 1 document set in advance and configure the platform to enable access automatically upon NDA confirmation. Tier 2 and Tier 3 folders should remain inaccessible until the appropriate process milestone is reached.

How long does it take to properly prepare a virtual data room?

For a lower-middle-market business in the $5M — 30M enterprise value range, a properly organized VDR typically requires eight to sixteen weeks to prepare from scratch, assuming the advisory team is starting the document collection process simultaneously. Businesses that maintain organized financial records, have formal contracts with material customers and vendors, and have previously completed an audit or financial review will typically fall at the shorter end of that range.

Businesses with informal record-keeping practices, undocumented IP, or complex multi-entity structures will take longer.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.