WACC Cost Allocations

WACC aggregates the costs of equity and debt based on their weights in the capital structure to establish the corporate cost of capital.

Estimate your company's discount rate. Model cost of equity via CAPM, factor in tax shields on corporate debt, and determine your weighted cost of capital.

Estimate Corporate Cost of Capital & Discount Rates

Strategic corporate acquirers and private equity sponsors use WACC to discount future cash flows. A higher WACC results in a compressed business valuation range.

Get an instant AI WACC diagnostic identifying debt optimization margins and market risk offsets.

WACC aggregates the costs of equity and debt based on their weights in the capital structure to establish the corporate cost of capital.

Equity holders require risk-adjusted returns calculated via CAPM, factoring in beta, risk-free interest, and market premiums.

Since interest is tax-deductible, corporate debt creates a tax shield, reducing the net cost of debt financing below the nominal interest rate.

WACC equals the weighted cost of equity plus the after-tax weighted cost of debt. Use equity value, debt value, tax rate, cost of equity, and cost of debt to estimate the discount rate for DCF and M&A valuation work.

When corporate acquirers, investment banks, or private equity sponsors evaluate a company, they model future cash generations using a Discounted Cash Flow (DCF) framework. To bring those future cash flows back to a present day dollars valuation, a risk-adjusted discount rate is required. This baseline benchmark is the **Weighted Average Cost of Capital (WACC)**.

A lower WACC discount rate mathematically increases the present value of future cash flows, driving a higher Enterprise Value (EV) and higher valuation multiples. Conversely, an elevated cost of capital compresses valuation multiples, making pre-sale WACC optimization a high-leverage move for sell-side advisors.

WACC calculates the blended costs of financing a company's assets across its primary capital channels: Equity and Debt. The equation weights each component relative to its overall proportion in the capital structure:

Where:

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.

The Cost of Equity (Ke) is highly sensitive to the systematic risk profile of the business, measured by Beta (尾).

Ein WACC Rechner berechnet die gewichteten Kapitalkosten aus Eigenkapitalkosten, Fremdkapitalkosten, Steuerquote und Kapitalstruktur. Das Ergebnis dient als Diskontierungszinssatz fuer DCF-Modelle und Unternehmensbewertungen.

Fuer M&A-Berater, Wirtschaftspruefer und Corporate-Finance-Teams im deutschsprachigen Raum ist die praezise Ermittlung der gewichteten durchschnittlichen Kapitalkosten ein fundamentaler Bestandteil jeder Unternehmensbewertung. Dieser WACC Rechner Online ermoeglicht eine schnelle Berechnung des Abzinsungssatzes fuer DCF-Modelle.

Geben Sie die Eigenkapitalkosten, die Fremdkapitalkosten nach Steuern sowie die jeweiligen Anteile am Gesamtkapital ein. Das Tool liefert ein klares WACC-Ergebnis fuer Bewertungs- und Investitionsszenarien.

Estimate the return required by shareholders using CAPM: risk-free rate plus beta multiplied by the equity risk premium.

Use the company's borrowing cost after the tax shield, because interest expense is generally tax deductible.

Weight equity and debt by target market value, not book value, so the discount rate matches buyer financing assumptions.

Run WACC sensitivities around the base case to show how discount rate assumptions affect enterprise value.

In M&A discussions, strategic buyers will attempt to use a high discount rate to depress their purchase offer. Sell-side advisors can defend premium valuations by modeling an optimal capital structure that balances tax-deductible debt weight against distress risk. Proving a normalized cost of capital validates the equity narrative, protecting enterprise cash multiples.

Quantify Enterprise Values, verify due diligence books, and estimate strategic synergy premiums in real-time.

Model Enterprise Value and EBITDA multiples based on cash-flow parameters.

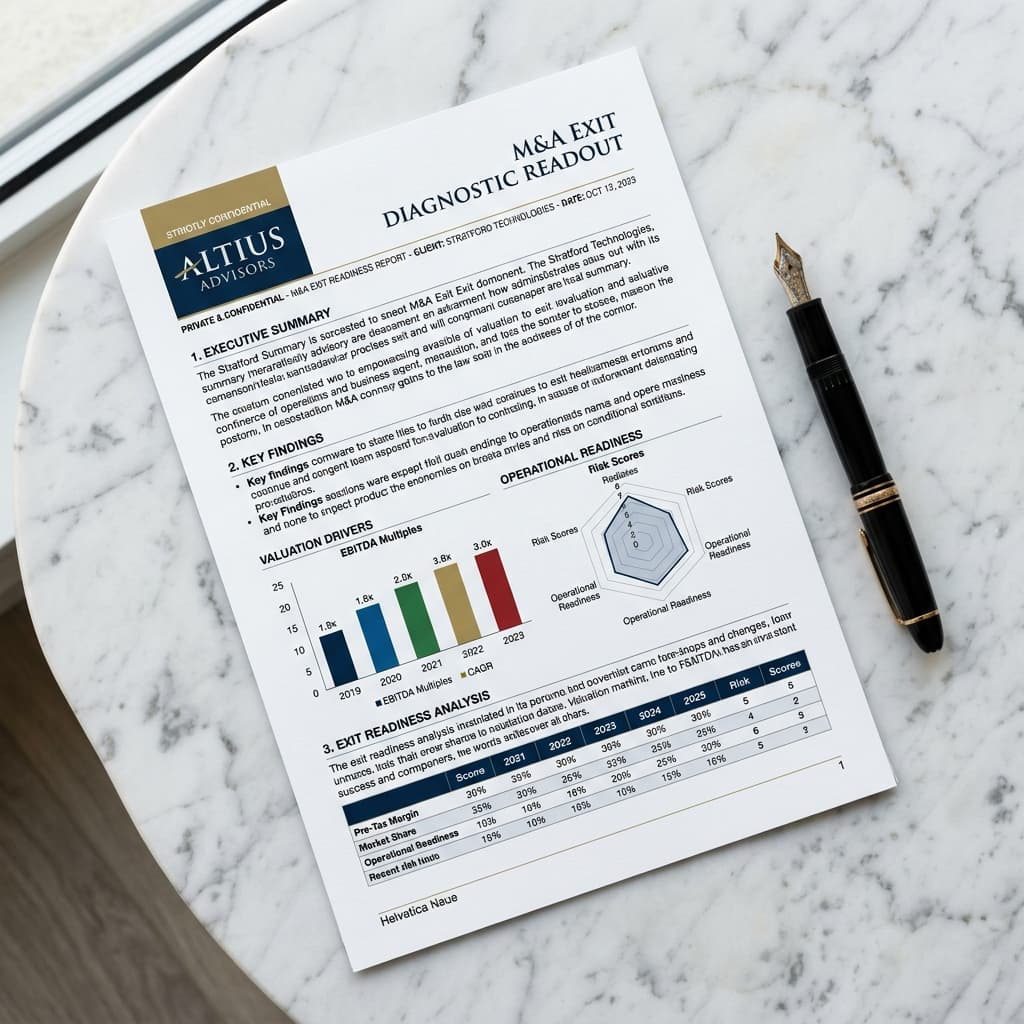

Reconcile VDR files and CIM statements to check QofE due diligence clawbacks.

Verify exit-readiness parameters, customer concentrations, and legal roadblocks.

Estimate annual cost reductions and customer cross-sell synergy values.

Leverage branded diagnostic assessments, AI drafting tools, and shared client collaboration channels.

Turn exit diagnostics into structured Confidential Information Memorandums automatically.

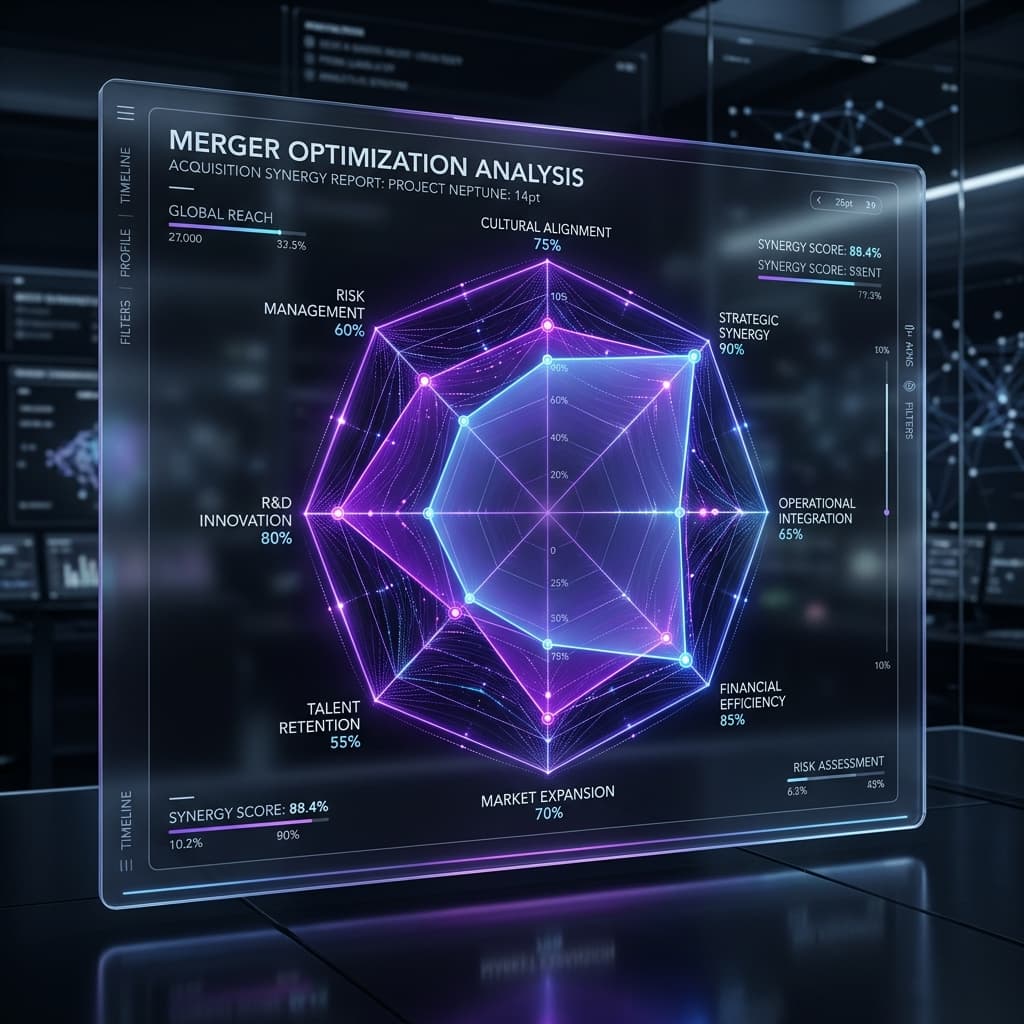

Mapstrategic buyer synergies and justify exit premium values across 6 dimensions.

Convert diagnostic risk findings into white-labeled seller remediation workflows.

Guide draft output tone with your boutique firm's custom brand vocabulary rules.

Read advanced articles written by tech corporate advisors covering escrow, EBITDA multiples, and transaction logs.

M&A Diligence

M&A DiligenceStep-by-step best practices to structure folders, manage user permissions, and ensure secure buyer access.

Valuation

ValuationA practical breakdown of valuation approaches owners and advisors use before a sale process.

Deal Structuring

Deal StructuringHow AI-assisted CIM workflows reduce drafting time while keeping deal materials consistent.