Normalizing Bridge

Calculators identify owner salaries, corporate travel, legal fees, or non-recurring vendor setup costs that buyers add back to build actual earnings power.

Reconcile your reported EBITDA to show buy-side private equity firms and strategic acquirers your company's true operational earnings power.

Verify Normalizing Add-backs & Deductions

Buyers challenge capitalized development offsets and owner lifestyle compensation normalization. Ensure you hold detailed audit ledgers to prevent valuation compression.

Get an instant AI audit analyzing potential buyer disputes on your EBITDA add-backs.

Calculators identify owner salaries, corporate travel, legal fees, or non-recurring vendor setup costs that buyers add back to build actual earnings power.

Adjust owner salaries to fair market replacement value. Replacing a founder with a salaried manager represents a major normalization step in small business sales.

Exclude one-time software re-licensing penalties, cybersecurity incidents, or legal settlement payouts from standard recurring operating expenses.

Reported financial statements for privately held companies often reflect owner-specific lifestyles or tax-minimization choices rather than the pure operating profitability of the business. In M&A processes, investment bankers and business brokers normalize EBITDA to isolate the true recurring cash flow of the business, yielding Adjusted EBITDA.

Common adjustments that increase the company's valuation bridge include:

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.

Every dollar of legitimate add-backs has a compounding effect on transaction value. If a business commands a 6.0x multiple, identifying an additional $50,000 of normalized owner add-backs raises the enterprise value by $300,000 at closing. Preparing a defensible Quality of Earnings (QofE) report beforehand is vital to prevent buyers from clawing back or retrading during diligence.

Buyers and their QofE accountants will systematically challenge normalization schedules. Common areas of buyer pushback include:

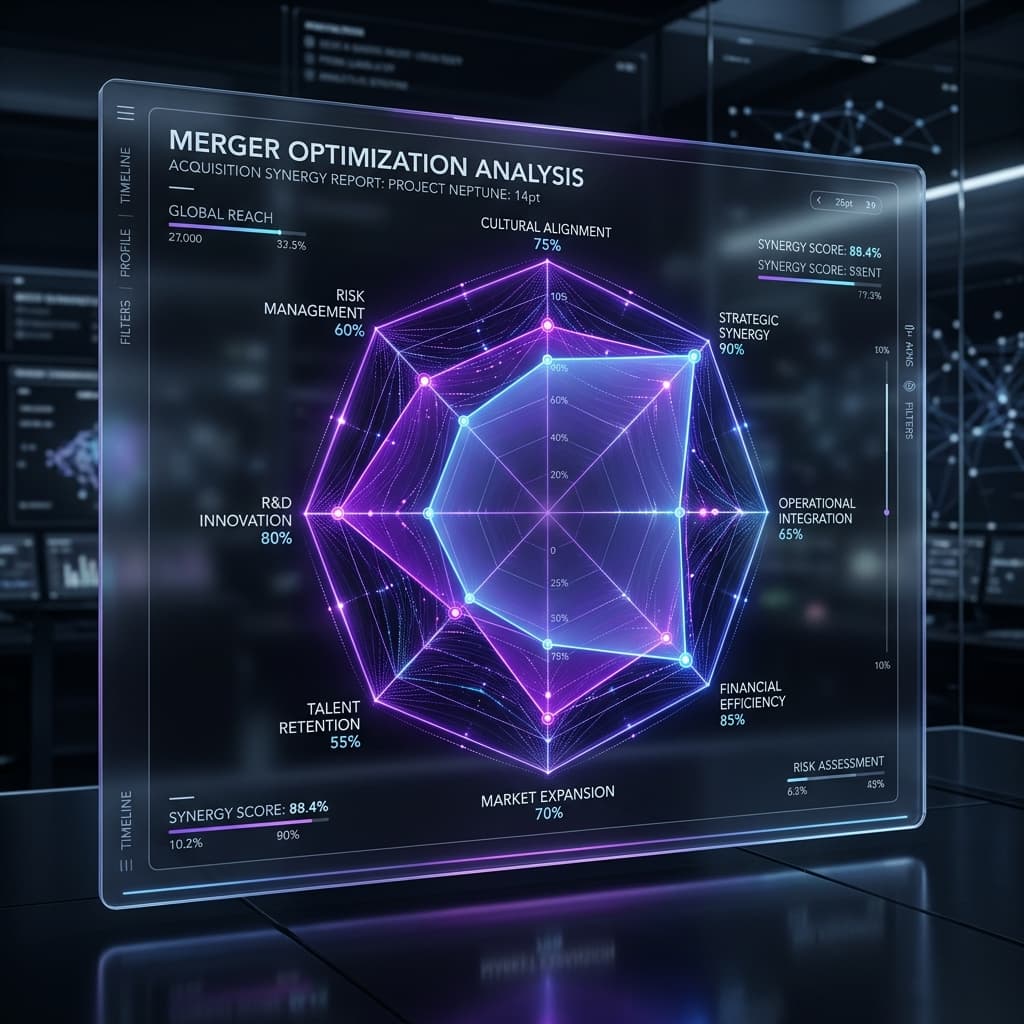

Quantify Enterprise Values, verify due diligence books, and estimate strategic synergy premiums in real-time.

Model Enterprise Value and EBITDA multiples based on cash-flow parameters.

Reconcile VDR files and CIM statements to check QofE due diligence clawbacks.

Verify exit-readiness parameters, customer concentrations, and legal roadblocks.

Estimate annual cost reductions and customer cross-sell synergy values.

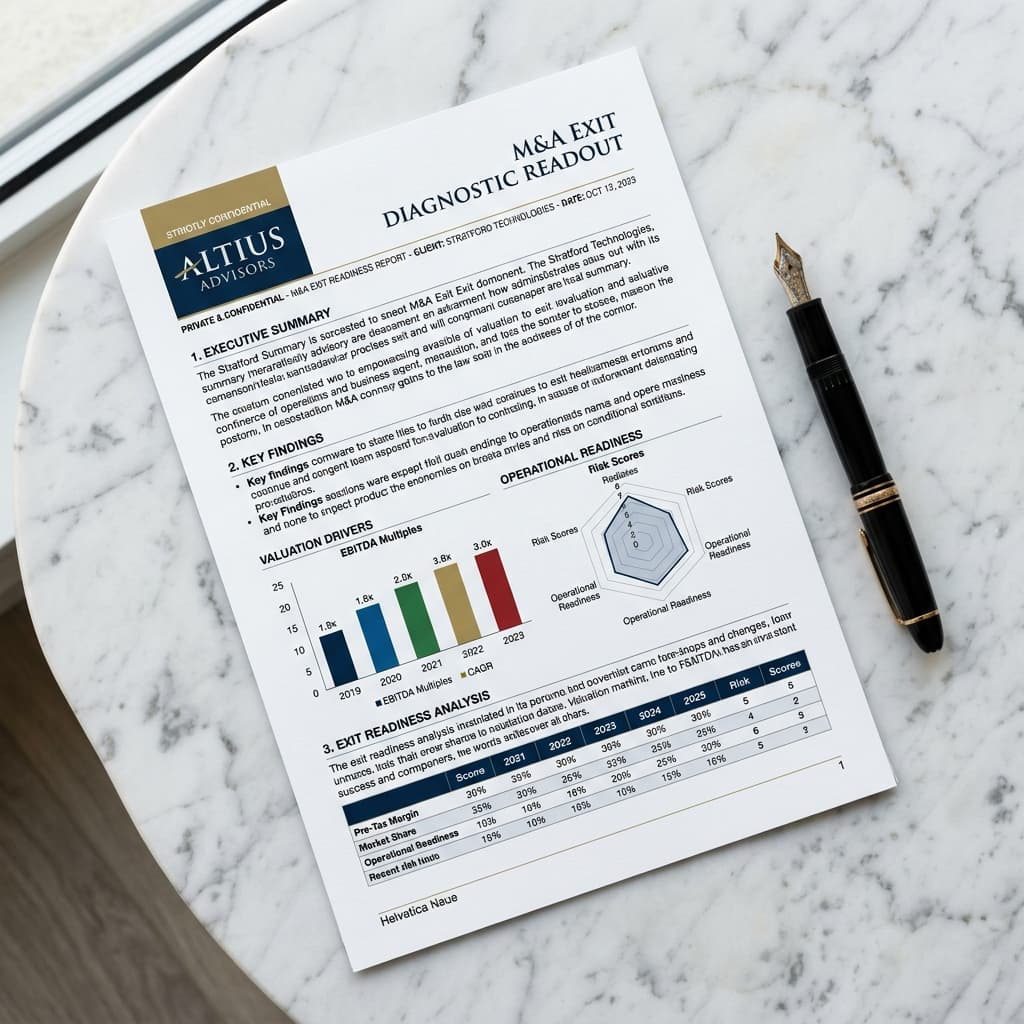

Leverage branded diagnostic assessments, AI drafting tools, and shared client collaboration channels.

Turn exit diagnostics into structured Confidential Information Memorandums automatically.

Mapstrategic buyer synergies and justify exit premium values across 6 dimensions.

Convert diagnostic risk findings into white-labeled seller remediation workflows.

Guide draft output tone with your boutique firm's custom brand vocabulary rules.

Read advanced articles written by tech corporate advisors covering escrow, EBITDA multiples, and transaction logs.

M&A Diligence

M&A DiligenceStep-by-step best practices to structure folders, manage user permissions, and ensure secure buyer access.

Valuation

ValuationA practical breakdown of valuation approaches owners and advisors use before a sale process.

Deal Structuring

Deal StructuringHow AI-assisted CIM workflows reduce drafting time while keeping deal materials consistent.