How Long Does Due Diligence Take in M&A — A 2026 Timeline Guide for Advisors

How Long Does Due Diligence Take in M&A — A 2026 Timeline Guide for Advisors The seller called three weeks after receiving their first letter of intent. They had expected to be close to signing by now. Instead, the buyer's accounting firm had just submitted a second round of financial document

How Long Does Due Diligence Take in M&A — A 2026 Timeline Guide for Advisors

The seller called three weeks after receiving their first letter of intent. They had expected to be close to signing by now.

Instead, the buyer's accounting firm had just submitted a second round of financial document requests, the legal team had flagged a change-of-control clause in one of the company's top vendor agreements, and the originally projected closing date — which everyone had agreed on during the LOI signing — was looking increasingly optimistic.

"How long is this supposed to take — " the seller asked.

It is a question advisors hear regularly, and the honest answer is more complicated than most sellers want to hear at the start of a process. Due diligence timelines in the lower-middle market vary significantly based on factors that are partly within the seller's control and partly not.

The single most controllable variable — and the one that has the greatest impact on timeline — is how prepared the seller was before the first buyer document request arrived.

This guide provides a realistic, phase-by-phase breakdown of M&A due diligence timelines in 2026, along with a clear explanation of what extends timelines, what compresses them, and what advisors can do to keep their clients on track.

Free Resource: Start your timeline on the right foot with a complimentary due diligence evaluation report — identify gaps before buyer access begins and set a realistic preparation schedule with your advisory team.

Why Most Sellers Underestimate How Long Due Diligence Takes

There is a consistent pattern in how sellers think about M&A timelines at the start of an engagement. They have heard that deals take three to six months.

They have mentally anchored on three. Their business plans, tax planning, and sometimes personal financial decisions are organized around a three-month assumption.

In practice, the confirmatory diligence phase alone — the period after the LOI is signed and before the purchase agreement is executed — routinely runs eight to twelve weeks in lower-middle-market transactions. Add the marketing phase, the management presentation period, and the LOI negotiation window, and a realistic total process timeline for a well-prepared seller is typically five to seven months from the first buyer conversation to closing.

For sellers who were not prepared before the process launched, twelve months or longer is not unusual.

The gap between expectation and reality is not primarily caused by buyer slowness or advisor inefficiency. It is caused by document gaps discovered during confirmatory diligence that require time to remediate, legal issues that surface after the LOI is signed, and financial discrepancies between the marketing package and the data room records that force renegotiation of financial representations.

Every one of those issues is more manageable — and takes less time to resolve — when it is identified before buyers are in the room.

The 3 Variables That Most Affect Timeline

In our experience across lower-middle-market sell-side processes, three factors account for the majority of timeline variance:

Document preparation completeness — Sellers who have a fully organized, pre-packaged VDR before the process launches consistently reach closing faster than those who are assembling documents reactively during active diligence. The difference can be measured in weeks, not days.

Financial statement quality — Businesses with reviewed or audited financial statements completed by a reputable accounting firm move through financial diligence significantly faster than those relying on internally prepared or compiled statements. The buyer's quality of earnings team has fewer questions when the starting point is a clean audit.

Complexity of the legal and corporate structure — Multi-entity structures, complex cap tables, significant intellectual property portfolios, and multi-state regulatory compliance all add diligence scope. These factors are not inherently problematic, but they require more time to document and review.

What We Actually See In Deals: The single most reliable predictor of a long diligence process is not the complexity of the business — it is the absence of a centralized document management system before the engagement begins. When a company's key documents are spread across personal email accounts, shared drives, and legacy file servers with no single advisor able to produce a requested document within the same business day, every buyer request creates a multi-day delay. Across a typical diligence process with dozens of document requests, those delays accumulate into weeks.

Case Studies: Fast Close vs Extended Diligence

Case Study: The Nine-Month Process That Nearly Killed the Deal

A manufacturing company in the upper Midwest entered a sale process with an advisory team they had engaged approximately four weeks before the first buyer materials were distributed. The business had strong financials and a genuine buyer universe, and initial buyer interest was encouraging.

The problems began when the first buyer group entered confirmatory diligence. The company had been operating for over twenty years, and its corporate records had accumulated accordingly: board minutes were incomplete for several years, the cap table had not been formally updated to reflect a partial equity transfer that had occurred informally several years earlier, and three of the company's top customer contracts had been operating under expired master service agreements on auto-renewal terms that had never been documented in writing.

Each issue was resolvable. None of them were discovered until buyers were actively reviewing documents and flagging them as gaps.

Resolving the cap table issue required input from a shareholder who had relocated internationally and was difficult to reach. Getting the expired contracts formally extended required three rounds of negotiation with customers who had not expected to be asked to sign updated agreements during the middle of a busy operating year.

The transaction ultimately closed — but at a timeline that ran substantially beyond what anyone had projected when the LOI was signed. The extended process created real costs: the seller's management team was distracted from running the business for months longer than anticipated, and the seller's legal fees significantly exceeded the original estimate.

How It Should Be Done: 14 Weeks Start to Close

A contrasting situation involved a Southeast professional services company whose advisory team began the pre-sale preparation process eleven months before the target process launch date. The firm conducted a full corporate records review, commissioned a quality of earnings engagement with an independent accounting firm, and used a structured pre-launch VDR audit to identify and remediate document gaps over a six-month preparation period.

When the process launched, the buyer group that ultimately transacted moved through their confirmatory diligence phase in approximately six weeks — well ahead of the projected timeline. The buyer's legal team found no material gaps.

The accounting firm's QofE review confirmed the normalized EBITDA figures in the CIM without adjustment. The purchase agreement negotiations were straightforward because neither party had discovered anything during diligence that had not already been disclosed.

From the first buyer NDA to the closing wire, the total timeline was fourteen weeks. For a lower-middle-market transaction, that is a genuinely compressed timeline — and it was driven entirely by the quality of preparation that preceded the process launch.

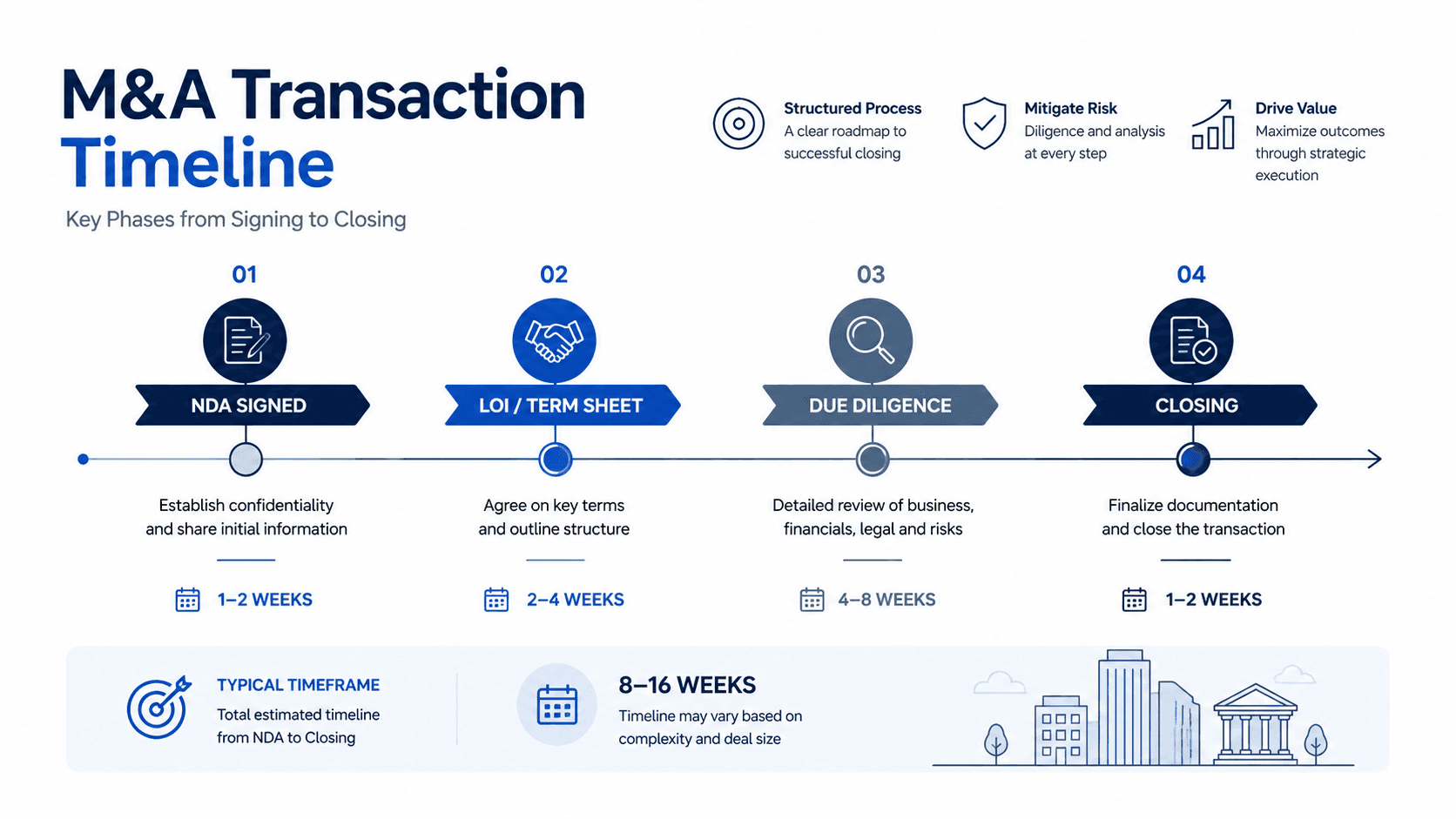

M&A Due Diligence Timeline: Phase-by-Phase Breakdown

Phase 1: NDA Execution and Initial Buyer Access (Weeks 1-2)

The formal diligence process begins when the first buyer signs a non-disclosure agreement and receives access to the teaser and CIM. During this phase, buyers are evaluating whether to invest the time and cost of deeper diligence.

They are reviewing the high-level financial profile, assessing strategic fit, and deciding whether to request a management presentation.

For sellers, this phase feels quiet but is operationally important. The advisory team is managing NDA execution for multiple buyer groups simultaneously, fielding initial questions, and coordinating the management presentation schedule for buyers who have expressed meaningful interest.

Timeline determinant: How quickly buyers can evaluate the CIM and decide to proceed depends heavily on CIM quality. A well-structured CIM that answers obvious buyer questions without prompting reduces the volume of preliminary questions and accelerates progression to the next phase.

Phase 2: Management Presentations and IOI Submission (Weeks 3-5)

Buyers who are seriously interested request a management presentation — typically a two-to-three-hour session where the seller's leadership team walks through the business in detail and takes questions from the buyer's deal team. Following the management presentation, serious buyers submit an Indication of Interest, which includes a preliminary valuation range and deal structure outline.

This phase is where the advisory team's process management skills matter most. Running three to five management presentations in a compressed window, maintaining competitive tension between buyer groups, and guiding the seller's leadership through the first substantive buyer interactions all happen simultaneously.

⚠️ The management presentation is also the first point at which financial figures are tested verbally. Sellers who present numbers that do not align with their data room records create doubt before confirmatory diligence even begins. Confirm that every figure discussed in the presentation can be traced to a specific document in the VDR before the first meeting.

Phase 3: LOI Negotiation and Exclusivity (Weeks 6-8)

After IOIs are submitted, the advisory team evaluates competing offers and selects a buyer to advance to exclusivity. The Letter of Intent negotiation typically covers purchase price, deal structure, exclusivity period, conditions to closing, and key representations.

LOI negotiation in the lower-middle market commonly takes one to three weeks depending on the complexity of the deal structure and the alignment between buyer and seller on key terms.

Once the LOI is signed, the seller enters an exclusivity period — typically 45 to 90 days — during which they are contractually restricted from engaging with other buyers. This exclusivity window is the confirmatory diligence phase, and it is where the clock matters most.

An exclusivity period that expires before diligence is complete requires either renegotiation or a decision to terminate the process.

Managing this window effectively requires that the seller's team be able to respond to buyer document requests quickly and completely from the first day of exclusivity.

Phase 4: Confirmatory Diligence, Purchase Agreement, and Closing (Weeks 9-14+)

Confirmatory diligence is the most intensive phase. The buyer's accounting firm conducts a quality of earnings review.

Legal counsel reviews all material contracts, corporate records, and compliance documentation. Operational due diligence may include site visits, management interviews, and customer reference calls.

During this phase, the purchase agreement is negotiated in parallel with ongoing diligence. The representations and warranties, indemnification provisions, working capital mechanism, and any escrow arrangements are all negotiated based on what the buyer finds — or does not find — during diligence.

For well-prepared sellers, this phase runs four to six weeks. For sellers with document gaps or financial discrepancies, it can run significantly longer as each issue is identified, investigated, and resolved.

According to IRS guidance on business sale tax considerations, sellers also need sufficient time before closing to address tax structure decisions that affect net proceeds — another reason early preparation matters.

Prepared VDR vs Unprepared VDR: Impact on Total Timeline

Fully Prepared VDR (Pre-Launch Audit Completed)

- Confirmatory diligence duration: 4-6 weeks

- Buyer document requests: Low volume; most materials available day one of access

- QofE review: Efficient; financial records align with CIM figures

- Legal review: Focused on material agreements; no time lost locating basic corporate records

- LOI retrades: Less frequent; fewer surprises discovered after exclusivity begins

- Total process timeline: 14-20 weeks from first NDA to closing

- Seller management distraction: Contained; leadership can focus on operations

Unprepared VDR (Assembled Reactively During Process)

- Confirmatory diligence duration: 10-16 weeks or longer

- Buyer document requests: High volume; multiple rounds required for basic materials

- QofE review: Extended; accountants identify CIM-to-VDR discrepancies requiring explanation

- Legal review: Broad and time-consuming; missing documents trigger follow-up requests

- LOI retrades: More frequent; buyers use discovered issues to renegotiate price or terms

- Total process timeline: 24-30+ weeks from first NDA to closing

- Seller management distraction: Significant; leadership pulled into diligence support for months

How AIVI Compresses Diligence Timelines for Boutique Advisors

Timeline compression in lower-middle-market M&A is fundamentally a preparation problem. Advisors who begin working through an exit readiness checklist six to twelve months before the process launch consistently see shorter confirmatory diligence windows and fewer post-LOI renegotiations. The deals that close quickly are the ones where the seller's advisory team had identified and addressed document gaps, financial discrepancies, and legal exposure before the first buyer logged into the data room.

Advisory teams using the VDR remediation Kanban at AIVI build this preparation process into a structured workflow rather than treating it as an ad-hoc pre-launch checklist. When a client completes the exit readiness diagnostic, the platform generates a structured gap analysis across all major diligence categories — the same categories that will consume the buyer's team during confirmatory diligence.

Each gap becomes an assigned task on the remediation board, tracked to completion with a target date linked to the VDR launch window.

The connection between preparation quality and timeline performance is direct. Review the complete due diligence checklist to understand what a fully prepared VDR should contain across all five document categories.

Use the VDR preparation guide to build the folder taxonomy and access control structure before the first buyer NDA is signed.

Both resources integrate with the AIVI remediation workflow, so the gap analysis, document tracking, and preparation timeline are managed in one place rather than across separate spreadsheets and email threads.

Frequently Asked Questions

How long does due diligence take for a small business sale?

For small business sales in the $1M-$5M enterprise value range, due diligence typically runs four to eight weeks for confirmatory diligence if the seller is prepared. The total process from first buyer contact to closing commonly runs three to five months.

Smaller transactions generally involve simpler corporate structures and lower document volumes, but they are also more likely to involve sellers who have not maintained formal financial records or executed written contracts with key customers and vendors, which extends the timeline.

What causes due diligence to take longer than expected?

The most common causes of extended diligence timelines are document gaps that require time to remediate after buyers identify them, financial statement discrepancies that require investigation and explanation, legal issues such as change-of-control clauses or missing IP documentation that surface during attorney review, and corporate structure complexities such as multiple entities, informal equity arrangements, or unresolved historical matters. All of these are more manageable when identified before the process launches rather than during active buyer review.

Can the due diligence timeline be shortened?

Yes, significantly. The most effective timeline compression strategies are beginning document preparation six to twelve months before the process launch, commissioning an independent quality of earnings review before marketing begins, conducting a pre-launch VDR audit to identify and remediate document gaps, and organizing all materials in a tiered, buyer-ready VDR structure before the first NDA is signed.

Sellers who complete these steps consistently experience shorter confirmatory diligence periods and fewer post-LOI negotiations than those who begin preparing after the first buyer conversation.

What happens if the exclusivity period expires before diligence is complete?

When an exclusivity period expires before confirmatory diligence is complete, the buyer and seller have three options: extend the exclusivity period by mutual agreement, which most buyers will agree to if progress is being made in good faith; allow exclusivity to lapse and continue the process on a non-exclusive basis, which gives the seller the ability to re-engage other buyers but may reduce the current buyer's urgency; or terminate the process, which is typically the outcome when the diligence findings have materially changed the buyer's view of the transaction. Preventing exclusivity expiration is one of the primary reasons pre-launch preparation matters — a well-organized VDR dramatically reduces the likelihood of diligence extending beyond the exclusivity window.

What is the difference between due diligence and a quality of earnings review?

Due diligence is the broad term for the full buyer investigation of a business before acquisition — it encompasses financial, legal, operational, and commercial review. A quality of earnings review (QofE) is a specific financial diligence engagement, typically conducted by an independent accounting firm retained by the buyer, that examines the quality, sustainability, and accuracy of the seller's reported earnings.

The QofE confirms or adjusts the EBITDA figure that the purchase price is based on. It is one component of the broader diligence process and is typically the most impactful single deliverable in determining whether the original LOI price holds through to closing.

Disclaimer: The financial and legal information provided in this article does not, and is not intended to, constitute professional legal or financial advice; instead, all information, content, and materials available on this site are for general informational purposes only. Readers should contact their legal counsel or certified public accountant to obtain advice with respect to any particular transaction or regulatory matter.

Ready to automate M&A drafting & secure transaction readiness?

AIVI empowers boutique M&A firms and investment banks to generate CIMs, conduct instant VDR gap checks, and manage exit readiness automatically from a unified data model.